Nvidia’s NVDA beat-and-raise quarterly outcomes have eased the market’s AI-centric worries for now, however the problem is unlikely to go away utterly.

The chipmaker has been a giant beneficiary of the continued AI-focused spending surge, as it’s Nvidia’s graphics processing items which can be operating the datacenters. The inventory has misplaced floor because the aforementioned worries took maintain at the beginning of this month, however it’s nonetheless up greater than +35% this 12 months, handily outperforming the broader market.

The broader Magazine 7 group, of which Nvidia is a key member, has returned largely in-line with the broader market, up +13.7% vs. a achieve of +14.1% for the S&P 500 index. The market doesn’t look like equally fearful about all AI gamers within the ongoing pullback, with Alphabet GOOGL persevering with to get credit score for its efforts at the same time as Meta META and a few of the others get shunned.

Nvidia’s Q3 earnings have been up +57.3% from the identical interval final 12 months on +62.5% increased revenues, placing the corporate on observe to greater than double its full-year 2025 earnings from the year-earlier degree. Earnings for subsequent 12 months are presently anticipated to be up +55%, adopted by +26.7% development in 2027.

This seemingly decelerating development development is solely a operate of base results, as demand traits for Nvidia’s chips stay crimson sizzling over the following two years. Demand will ultimately reasonable as we transfer previous the buildout section of AI infrastructure, and the inventory’s current weak point is probably going a mirrored image of that.

One may argue that the inventory’s spectacular good points over the previous few years, that has pushed its market capitalization to over $4 trillion, have already factored in these expectations. But when estimates preserve rising, as we’re beginning to see once more following the beat-and-raise quarterly outcomes, then Nvidia shareholders will legitimately anticipate the inventory to maintain its optimistic trajectory. You possibly can see Nvidia’s enviable estimate revisions development within the beneath Worth, Consensus & Shock chart.

Picture Supply: Zacks Funding Analysis

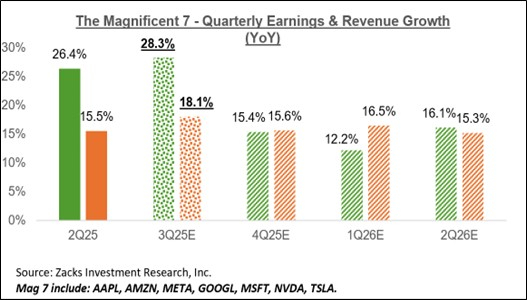

Together with Nvidia, the Magazine 7 group’s Q3 earnings elevated +28.3% from the identical interval final 12 months on +18.1% increased revenues, which might comply with the group’s +26.4% earnings development on +15.5% income development.

Not all members of the elite group are equally contributing to the expansion tempo, starting from Tesla’s TSLA -39.5% earnings decline in Q3 to Nvidia’s +57.3% leap and Alphabet’s GOOGL +33% development tempo.

The chart beneath exhibits the group’s blended Q3 earnings and income development relative to what was achieved within the previous interval and what’s anticipated within the coming three durations.

Picture Supply: Zacks Funding Analysis

Estimates for the present interval (2025 This autumn) are going up, with the present earnings development price of +15.4% up from +14.3% per week again and +12.2% two weeks in the past.

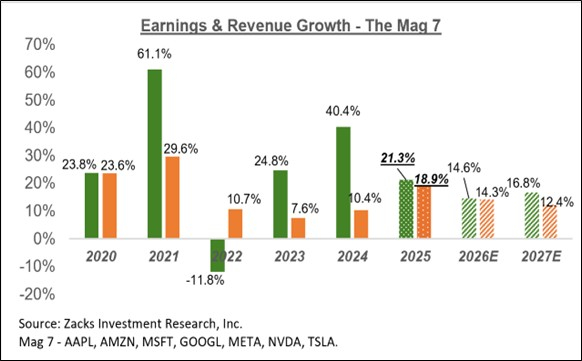

The chart beneath exhibits the Magazine 7 group’s earnings and income development image on an annual foundation.

Picture Supply: Zacks Funding Analysis

As you possibly can see above, the group’s 2026 earnings are presently anticipated to be up +14.6%, adopted by +16.8% in 2027.

The essential issue to remember is that the Magazine 7 earnings outlook is steadily enhancing, because the chart beneath exhibits.

Picture Supply: Zacks Funding Analysis

Please be aware that the Magazine 7 group is on observe to herald 26% of all S&P 500 earnings in 2026, up from 23.2% of the full in 2024 and 11.7% in 2019. Relating to market capitalization, the Magazine 7 group presently carries a 34.7% weight within the index.

Q3 Earnings Season Scorecard

Together with all reviews launched via Friday, November twenty first, we now have Q3 outcomes from 473 S&P 500 members, or 94.8% of the index’s complete membership. The reporting cycle has come to an finish for 10 of the 16 Zacks sectors, with many of the remaining outcomes from the Tech and Retail sectors.

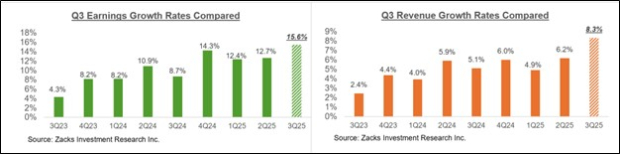

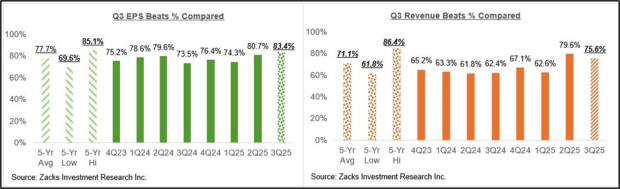

Whole earnings for these corporations are up +15.6% from the identical interval final 12 months on +8.3% increased revenues, with 83.4% beating EPS estimates and 75.6% beating income estimates.

The comparability charts beneath put the Q3 earnings and income development charges from these corporations in a historic context.

Picture Supply: Zacks Funding Analysis

The comparability charts beneath present the Q3 EPS and income beats percentages in a historic context.

Picture Supply: Zacks Funding Analysis

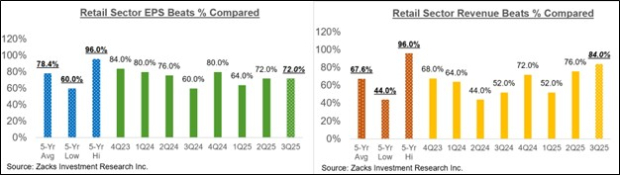

For the Retail sector, we now have Q3 outcomes for 83.3% of the sector’s members within the S&P 500 index. Whole earnings for these Retail corporations are up +16.9% from the identical interval final 12 months on +7.7% increased revenues, with 72% beating EPS estimates and 84% beating income estimates.

The comparability charts beneath present the sector’s Q3 EPS and income beats percentages in a historic context.

Picture Supply: Zacks Funding Analysis

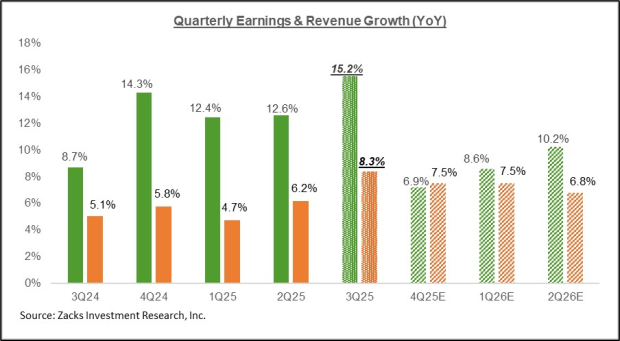

The comparability charts beneath present the sector’s Q3 earnings and income development charges in a historic context. We like to point out the Retail sector’s development comparisons with and with out Amazon’s outcomes, given the e-commerce big’s huge heft. The chart on the best facet exhibits the sector’s Q3 earnings and income development efficiency with out Amazon’s contribution.

Picture Supply: Zacks Funding Analysis

The Earnings Huge Image

The chart beneath exhibits present Q3 earnings and income development expectations for the S&P 500 index within the context of the previous 4 quarters and the approaching 4.

Picture Supply: Zacks Funding Analysis

Please be aware that the +15.2% earnings development price for Q3 proven above represents the blended development price for the quarter, which mixes the precise outcomes for the 473 corporations which have reported with estimates for the still-to-come corporations.

The chart beneath exhibits the general earnings image on a calendar-year foundation.

Picture Supply: Zacks Funding Analysis

By way of S&P 500 index ‘EPS’, these development charges approximate to $261.68 for 2025 and $292.52 for 2026. The chart beneath exhibits how subsequent 12 months’s index ‘EPS’ estimate has developed for the reason that begin of the second half of the 12 months

Picture Supply: Zacks Funding Analysis

For an in depth view of the evolving earnings image, please take a look at our weekly Earnings Traits report right here >>>>Q3 Earnings Season: Retail Sector in Focus

5 Shares Set to Double

Every was handpicked by a Zacks skilled because the #1 favourite inventory to realize +100% or extra within the coming 12 months. Whereas not all picks will be winners, earlier suggestions have soared +112%, +171%, +209% and +232%.

Many of the shares on this report are flying beneath Wall Avenue radar, which gives an ideal alternative to get in on the bottom ground.

Right now, See These 5 Potential Residence Runs >>

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

Tesla, Inc. (TSLA) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.

")