The Procter & Gamble Firm’s PG first quarter of fiscal 2026 painted an image of combined regional dynamics, regular however slowing progress in North America and a promising rebound in China. The patron items big reported 2% natural gross sales progress, led by sturdy momentum in pores and skin, private and child care classes. Nonetheless, the U.S. market — lengthy PG’s cornerstone — confirmed indicators of fatigue as shopper spending softened and promotional depth elevated throughout key classes like Cloth and Child Care. Administration acknowledged that consumption in North America decelerated by way of the quarter to below 2%, a mirrored image of cautious customers and heightened competitors.

In distinction, Higher China emerged as a brilliant spot. Natural gross sales within the area climbed 5%, marking one other quarter of sequential enchancment and signaling that PG’s strategic interventions are taking maintain. The corporate’s efforts to revamp its distributor mannequin, elevate model innovation and tailor choices to native shopper insights have pushed broad-based progress, notably in premium segments like SK-II and Olay, in addition to double-digit positive factors in Child Care. Regardless of lingering macro volatility, the corporate’s renewed deal with localized innovation and premiumization seems to be restoring momentum on this essential market.

Going ahead, Procter & Gamble faces the duty of rebalancing progress between mature and rising areas. Whereas North America stays pressured, the corporate is intensifying innovation and worth efforts whereas channeling restructuring financial savings towards high-growth markets like China and Latin America. This method positions PG to offset U.S. softness and maintain balanced world efficiency.

PG’s Friends: How CHD & CL Navigate Slowing International Demand

In as we speak’s inflationary and risky surroundings, each Church & Dwight CHD and Colgate-Palmolive Firm CL are navigating slowing world demand with strategic self-discipline.

Church & Dwight is balancing slower class progress by way of its diversified model portfolio and deal with value-oriented innovation. The corporate advantages from its publicity to each premium and on a regular basis necessities, cushioning demand fluctuations. CHD has leaned into strategic price-pack structure, productiveness initiatives and selective acquisitions to maintain profitability. Whereas inflation and softer shopper sentiment weigh on volumes, the corporate’s sturdy execution, disciplined pricing and advertising funding in core manufacturers proceed to help resilient earnings efficiency in a difficult world surroundings.

Colgate is navigating the slowdown in world demand by leaning on its core strengths in oral care and premium innovation. The corporate continues to ship regular progress by way of pricing actions, portfolio premiumization and increasing digital engagement, at the same time as volumes stay pressured in some markets. Its innovation pipeline, highlighted by high-performance toothpaste and sustainable packaging, has helped preserve model loyalty and pricing energy. Whereas rising markets like Latin America and India proceed to drive stable momentum, Colgate can also be specializing in value self-discipline and productiveness positive factors to guard margins amid macro headwinds and international trade volatility.

PG’s Value Efficiency, Valuation & Estimates

Procter & Gamble’s shares have misplaced round 12.3% yr so far in contrast with the industry’s 11.9% dip.

Picture Supply: Zacks Funding Analysis

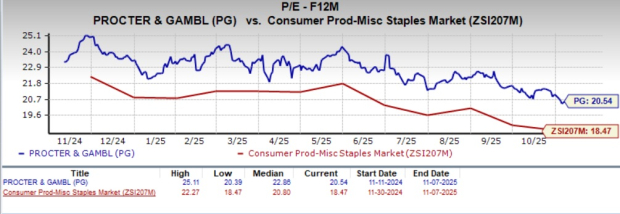

From a valuation standpoint, PG trades at a ahead price-to-earnings ratio of 20.54X in contrast with the trade’s common of 18.47X.

Picture Supply: Zacks Funding Analysis

The Zacks Consensus Estimate for PG’s fiscal 2025 and 2026 EPS signifies year-over-year progress of two.6% and 5.7%, respectively. The corporate’s EPS estimates for fiscal 2025 have moved upward, whereas estimates for fiscal 2026 have remained secure previously 30 days.

Picture Supply: Zacks Funding Analysis

Procter & Gamble presently carries a Zacks Rank #3 (Maintain). You may see the entire record of as we speak’s Zacks #1 Rank (Robust Purchase) shares right here.

5 Shares Set to Double

Every was handpicked by a Zacks professional as the favourite inventory to realize +100% or extra within the months forward. They embrace

Inventory #1: A Disruptive Drive with Notable Development and Resilience

Inventory #2: Bullish Indicators Signaling to Purchase the Dip

Inventory #3: One of many Most Compelling Investments within the Market

Inventory #4: Chief In a Pink-Scorching Business Poised for Development

Inventory #5: Trendy Omni-Channel Platform Coiled to Spring

Many of the shares on this report are flying below Wall Road radar, which offers an ideal alternative to get in on the bottom ground. Whereas not all picks could be winners, earlier suggestions have soared +171%, +209% and +232%.

Obtain Atomic Alternative: Nuclear Vitality’s Comeback free as we speak.

Procter & Gamble Firm (The) (PG) : Free Inventory Evaluation Report

Colgate-Palmolive Firm (CL) : Free Inventory Evaluation Report

Church & Dwight Co., Inc. (CHD) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.

")