Realty Earnings Corporation O, a pacesetter within the web lease sector, is slated to launch third-quarter 2025 outcomes on Nov. 3, after market shut. The Zacks Consensus Estimate for the to-be-reported quarter’s adjusted funds from operations (AFFO) and revenues is pegged at $1.07 per share and $1.42 billion, respectively.

The Zacks Consensus Estimate for third-quarter 2025 AFFO per share has remained unrevised at $1.07 over the previous two months. It suggests 1.90% development yr over yr. The Zacks Consensus Estimate for quarterly revenues implies a notable year-over-year improve of 6.61%.

Picture Supply: Zacks Funding Analysis

For the present yr, the Zacks Consensus Estimate for Realty Earnings’s revenues is pegged at $5.63 billion, implying an increase of 6.72% yr over yr. The consensus mark for 2025 AFFO per share stands at $4.27, calling for an growth of round 1.91% on a year-over-year foundation.

Over the trailing 4 quarters, the corporate’s AFFO per share met the Zacks Consensus Estimate on two events for as many misses. That is depicted within the graph under:

Realty Earnings Company Worth and EPS Shock

Realty Earnings Company price-eps-surprise | Realty Earnings Company Quote

Right here Is What Our Quantitative Mannequin Predicts for O

Our confirmed mannequin predicts a shock when it comes to AFFO per share for Realty Earnings this season. The mix of a optimistic Earnings ESP and a Zacks Rank #1 (Sturdy Purchase), 2 (Purchase) or 3 (Maintain) will increase the possibilities of an AFFO beat, which is the case right here. You may see the whole listing of right this moment’s Zacks #1 Rank shares here.

Realty Earnings presently carries a Zacks Rank of three and has an Earnings ESP of +0.37%. You may uncover the very best shares to purchase or promote earlier than they’re reported with our Earnings ESP Filter.

Realty Earnings’s Q3 Doubtless Marked by Stability and Energy

Realty Earnings is more likely to have witnessed secure operational efficiency within the third quarter of 2025, pushed by its well-diversified, high-quality property portfolio. A big share of its rental revenues comes from tenants with non-discretionary, low worth level and service-oriented focus, supporting regular money movement. Its disciplined acquisition technique and emphasis on high-performing belongings possible continued to underpin portfolio energy and operational consistency through the interval.

As of June 30, 2025, the corporate reported a powerful 98.6% occupancy fee, which is predicted to have remained above 98% by way of the third quarter. This sustained occupancy, reflecting prudent underwriting and resilient tenant demand, is more likely to have supported earnings stability. Realty Earnings’s concentrate on defensive sectors and proactive asset administration is believed to have additional enhanced portfolio sturdiness.

The corporate can be anticipated to have benefited from ongoing diversification past retail into industrial, gaming, and knowledge heart belongings. Its partnership with Digital Realty DLR highlights its forward-focused method, supporting entry into the rising digital infrastructure house. Other than its collaboration with Digital Realty, it’s eyeing growth in Europe and is concentrating on $5 billion in investments for 2025.

On the steadiness sheet entrance, the corporate is more likely to have maintained a powerful monetary footing, backed by investment-grade credit score scores of A3 from Moody’s and A- from S&P. Its capital construction is predicted to have remained sound, with manageable leverage, a well-laddered debt maturity profile, and ample liquidity, all of that are more likely to have enhanced flexibility to fund development and handle refinancing danger.

The consensus mark for rental revenues (excluding reimbursable) is pegged at $1.28 billion, up from $1.25 billion recorded within the prior quarter and $1.20 billion within the year-ago quarter.

Regardless of its strengths, Realty Earnings faces sure challenges. The corporate’s 2025 steerage elements in roughly 75 foundation factors of anticipated lease loss, above historic norms, primarily stemming from tenants added by way of earlier mergers and acquisitions. The presence of financially weaker tenants introduces near-term uncertainty and should put stress on money movement reliability.

O’s Worth Efficiency & Valuation

Shares of Realty Earnings have rallied 8.4% up to now within the yr, closing at $57.91 yesterday on the NYSE. The Zacks REIT and Fairness Belief – Retail business has declined 6.6%, whereas the S&P 500 composite has elevated 18.6% over the identical timeframe.

YTD Worth Efficiency

Picture Supply: Zacks Funding Analysis

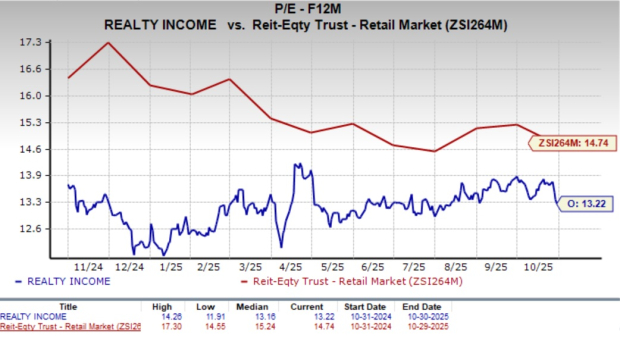

Valuation-wise, Realty Earnings trades at a ahead price-to-FFO of 13.22X, under the retail REIT business common of 14.74X and barely above its one-year median of 13.16X. The inventory seems moderately priced versus its friends. It’s cheaper than Agree Realty Company ADC but considerably pricier than NNN REIT NNN. Agree Realty is buying and selling at a ahead 12-month price-to-FFO of 16.23X, whereas NNN is buying and selling at 11.59X. Nonetheless, its Worth Rating of D means that it is probably not a discount at present ranges.

Ahead 12 Month Worth-to-FFO (P/FFO) Ratio

Picture Supply: Zacks Funding Analysis

Tips on how to Play Realty Earnings Inventory Forward of Q3 Earnings

Realty Earnings continues to face out as a reliable income-oriented REIT, providing a powerful mix of stability and measured development. Its diversified portfolio, essential-service tenant combine, and long-term web lease construction underpin regular money flows, whereas growth into gaming and knowledge facilities by way of partnerships like Digital Realty enhances long-term relevance. The corporate’s 5.54% dividend yield and investment-grade steadiness sheet additional solidify its attraction for income-seeking buyers.

That stated, near-term development prospects stay tempered by macroeconomic uncertainty. With the inventory buying and selling at a modest low cost to friends comparable to Agree Realty, endurance could also be warranted till larger readability emerges on financial momentum.

Given its balanced risk-reward profile, it’s higher to carry Realty Earnings. Current buyers can proceed benefiting from its reliable dividends and defensive portfolio, whereas potential patrons could choose to attend for a extra engaging entry level.

Observe: Something associated to earnings introduced on this write-up represents funds from operations (FFO) — a extensively used metric to gauge the efficiency of REITs.

Digital Realty Belief, Inc. (DLR) : Free Inventory Evaluation Report

NNN REIT, Inc. (NNN) : Free Inventory Evaluation Report

Realty Earnings Company (O) : Free Inventory Evaluation Report

Agree Realty Company (ADC) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.