")

Trend is fickle, simply ask former Wall Avenue darling lululemon athletica inc. LULU. The athleisure energy, which modified vogue for a time period, is going through altering developments, elevated competitors, and different headwinds.

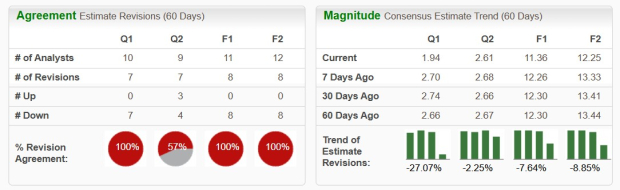

Lululemon’s earnings revisions went right into a downward spiral beginning in late 2024. Its earnings outlook took one other flip for the more severe after it reported its Q1 FY26 outcomes on June 4.

LULU’s most up-to-date downward earnings revisions earn the athletic attire maker a Zacks Rank #5 (Sturdy Promote). The inventory has additionally tanked 50% within the final 12 months.

Ought to Traders Keep Away from LULU Inventory Proper Now?

Lululemon is lastly going through slowing progress within the U.S. and North America after a banner stretch of enlargement that noticed it common 23% income progress between 2018 and 2023. The speedy enlargement of rivals Alo, Vuori, and numerous different online-only startups can also be contributing to LULU’s slowing comparable retailer gross sales in its essential Americas area.

On prime of that, broader vogue developments look like shifting away from Lululemon’s core choices. Regardless that LULU has actively expanded its enterprise in an effort to adapt, Wall Avenue is unconvinced it is able to flip issues round.

Picture Supply: Zacks Funding Analysis

LULU grew its FY25 income by 5%, marking by far its lowest ever YoY gross sales enlargement as a public firm. Earlier than that, 2024’s 10% income progress was its slowest 12 months of progress.

The corporate’s Americas comparable gross sales decreased 3% in fiscal 2025. Lululemon adopted up that tough efficiency in its most necessary market with a 5% YoY decline in Americas comps within the first quarter of FY26.

The corporate’s Q2 earnings estimate dropped roughly 27% since its report on June 4, with its FY26 estimate one other 8% decrease and FY27’s 9% off the tempo. The current downward revisions earn Lululemon a Zacks Rank #5 (Sturdy Promote), and lengthen its downward earnings spiral.

Lululemon is projected to develop its income by round 0.5% in FY26 and practically 5% subsequent 12 months. In the meantime, its adjusted earnings are anticipated to fall 14% YoY in FY26 after which leap 8% subsequent 12 months, primarily based on present Zacks estimates.

Picture Supply: Zacks Funding Analysis

LULU’s 40% YTD dive is a part of a ~75% drop from its early 2024 peaks. The autumn has it buying and selling the place it was in numerous components of 2018 and at its lowest ever ahead earnings a number of at 9.4X ahead 12-month EPS. This backdrop implies that traders ought to probably hold Lululemon on their watchlists and probably take a nibble at it when administration exhibits Wall Avenue {that a} turnaround is on the horizon.

Till then, traders ought to probably look elsewhere for shares to purchase throughout the attire business and past.

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t more likely to hold delivering the largest income. AI’s second wave is shifting from infrastructure to implementation and these firms are on the forefront of this transition, positioned to change into what Amazon and Google have been to the web period.

lululemon athletica inc. (LULU) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.