Meta Platforms META) inventory has endured a tough stretch just lately, with shares down 10% this month and off roughly 15% year-to-date.

The decline has come regardless of continued power throughout lots of the tech leaders’ core companies. To that time, Meta continues to be benefiting from highly effective aggressive benefits, together with its huge person base, in depth advertiser relationships, and powerful steadiness sheet.

Mixed with ongoing AI-driven alternatives, these strengths might assist long-term earnings enlargement.

This raises an essential query for traders: Has the latest selloff created a pretty alternative, or are there nonetheless causes for warning?

Picture Supply: Zacks Funding Analysis

Meta Continues to Dominate Digital Promoting

Meta stays probably the most influential gamers in digital promoting, supported by its huge household of apps that features Fb, Instagram, Messenger, and WhatsApp. Collectively, Meta continues to draw billions of each day customers worldwide, giving advertisers unparalleled attain and engagement alternatives.

Moreover, promoting demand has remained wholesome as firms more and more depend on digital channels to attach with shoppers. Meta’s superior focusing on capabilities and AI-driven advert instruments have additionally helped enhance marketing campaign effectiveness, supporting robust monetization tendencies throughout its platforms.

In consequence, Meta continues to generate substantial money stream and spectacular profitability regardless of ongoing investments in future development initiatives.

AI Investments Might Drive Lengthy-Time period Growth

Synthetic intelligence has develop into a serious focus for Meta, with administration aggressively investing in infrastructure, together with knowledge facilities and computing capability, to assist more and more refined AI fashions.

These investments should not solely meant to enhance the person expertise but additionally to boost promoting efficiency. On this regard, higher advice algorithms and more practical advert focusing on are serving to to extend engagement whereas boosting returns for advertisers.

As well as, Meta is exploring alternatives to combine AI throughout its product ecosystem, probably creating new income streams and strengthening its aggressive place over the long run.

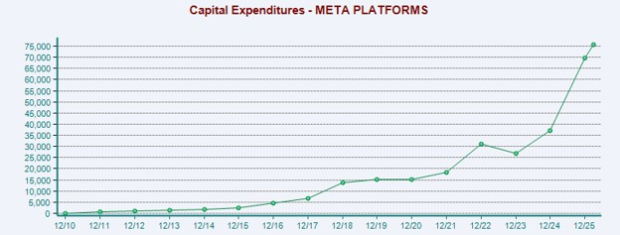

That stated, it is value noting that Meta expects spending to speed up even additional this yr, with 2026 capital expenditures projected between $115 billion-$135 billion, underscoring simply how aggressively the corporate is pursuing its AI technique.

Picture Supply: Zacks Funding Analysis

The Actuality Labs Query Stays

Whereas Meta’s core enterprise stays extremely worthwhile, traders proceed to carefully monitor the corporate’s Actuality Labs section.

The division, which homes Meta’s digital actuality and metaverse initiatives, has generated substantial working losses for a number of years. Though administration views these investments as important to the corporate’s future, the timing and magnitude of potential returns stay unsure.

Some traders fear that continued spending in the direction of its Actuality Labs division might stress margins and scale back earnings development, notably if financial circumstances weaken or promoting demand slows.

Analysts Nonetheless Anticipate Robust Development

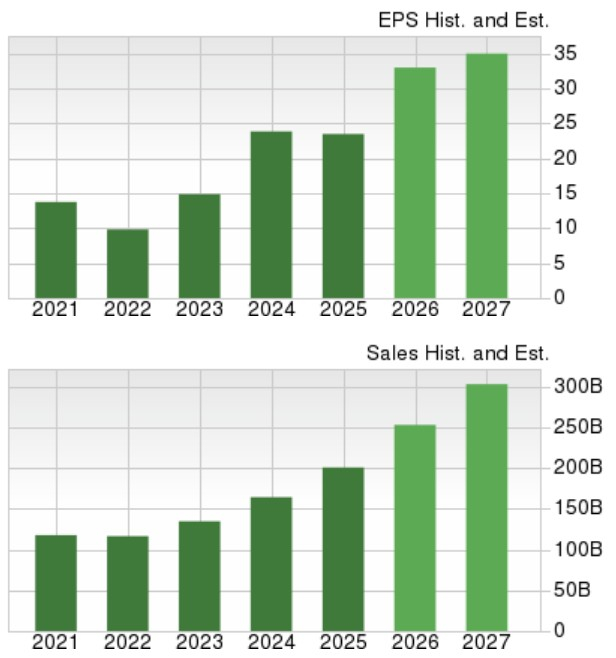

Regardless of latest weak point in Meta inventory, Wall Road continues to challenge wholesome development. The Zacks Consensus Estimate requires 2026 income of $253.28 billion, representing 26% development from the prior yr. Analysts at the moment count on income to climb one other 20% in 2027 to over $300 billion.

Whereas earnings development is anticipated to average, the consensus nonetheless requires Meta’s EPS to extend 40% this yr to $33.00, adopted by a 6% enhance in FY27 to $35.02.

Picture Supply: Zacks Funding Analysis

The Least expensive P/E Valuation Among the many Magazine 7

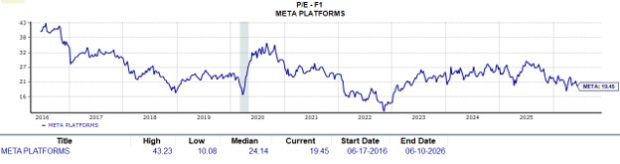

Following the latest decline, Meta now has the most cost effective P/E valuation among the many Magazine 7 at 19X ahead earnings, adopted by Microsoft MSFT) and Alphabet GOOGL) at 22X and 24X, respectively.

Extra intriguing, META is buying and selling at a 20% low cost to its decade-long median of 24X ahead earnings and is greater than 50% beneath its excessive of 43X throughout this era.

Picture Supply: Zacks Funding Analysis

Backside Line

Meta Platforms stays one of many highest-quality know-how firms available in the market, and the latest pullback might encourage extra traders to take a better have a look at its inventory. The corporate’s dominant promoting franchise, robust money technology, and rising AI capabilities present compelling long-term development drivers.

On the similar time, traders ought to acknowledge that Meta just isn’t with out dangers. Elevated capital expenditures, regulatory scrutiny, and uncertainty surrounding Actuality Labs might proceed to create volatility. For now, META lands a Zacks Rank #3 (Maintain).

7 Greatest Shares for the Subsequent 30 Days

Simply launched: Consultants distill 7 elite shares from the present record of 220 Zacks Rank #1 Robust Buys. They deem these tickers “Most Doubtless for Early Value Pops.”

Since 1988, the total record has overwhelmed the market greater than 2X over with a median achieve of +23.7% per yr. So make sure to give these hand picked 7 your fast consideration.

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.