")

Houlihan Lokey HLI) has lengthy been one of the revered names in impartial funding banking, however its inventory is now going through a significant shift in analyst sentiment.

Over the previous a number of weeks, earnings estimates have been shifting sharply decrease, with the downward pattern reflecting a mix of softer-than-expected monetary outcomes, weakening momentum in key enterprise traces, and cautious administration commentary.

With EPS revisions falling this broadly, Houlihan’s inventory has been flagged as a possible underperformer, touchdown a Zacks Rank #5 (Robust Promote) and the Bear of the Day.

Picture Supply: Zacks Funding Analysis

A Double Miss That Reset Expectations

Sparking considerations was Houlihan’s most up-to-date fiscal fourth-quarter report final month, the catalyst for what has been a wave of downward EPS revisions:

- This fall Income of $635.64 million missed the $687.1 million Consensus by 7% and fell 4% from the prior yr quarter.

- This fall EPS of $1.63 missed expectations of $1.84 by 11% and dropped from $1.96 a yr in the past.

Picture Supply: Zacks Funding Analysis

A miss on each the highest and backside line is normally sufficient to set off estimate cuts, however what involved analysts much more was that the weak spot confirmed up in Houlihan’s core Monetary Restructuring (FR) enterprise, which advises corporations, collectors, personal fairness sponsors, and different stakeholders when an organization is underneath monetary stress or must reorganize its steadiness sheet.

Restructuring Slowdown & Broad Underperformance

Finest recognized for its management in monetary restructuring, a phase that traditionally delivers a few of Houlihan’s highest margins, current declines have raised eyebrows.

To that time, This fall Restructuring income fell 33% YoY to $110.4 million and noticeably missed expectations of $137.2 million.

This can be a notable shift as a result of restructuring tends to growth in periods of broader financial uncertainty, which, after all, has been highlighted by elevated rates of interest and better vitality costs from the Warfare in Iran. That mentioned, the present restructuring surroundings has seen fewer large-scale misery conditions. With the cycle cooling, analysts are recalibrating their ahead assumptions.

Moreover, the weak spot wasn’t remoted to restructuring, as income for Houlihan’s Company Finance and Valuation Advisory segments additionally got here in beneath expectations:

- This fall Company Finance income: $433.8M vs. $448.8M anticipated

- This fall Valuation Advisory income: $91.5M vs. $95.5M anticipated

When each main enterprise line misses estimates, analysts are inclined to assume the softness is macro-driven and more likely to persist.

Administration’s Tone Provides to the Strain

Despite the fact that Houlihan nonetheless delivered a file fiscal yr, administration struck a noticeably cautious tone in regards to the near-term surroundings, citing “uncertainty” because the agency enters its FY27. When management alerts hesitation on high of current quarterly underperformance, analysts normally trim their outlook.

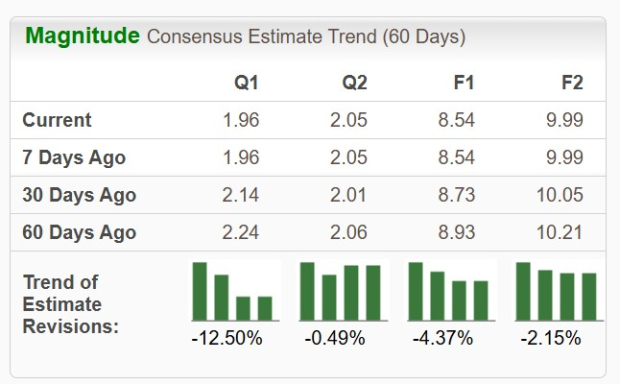

Analysts Reply With EPS Cuts

As proven beneath, Houlihan’s EPS revisions are beginning to decline throughout the board, highlighted by what’s now a 12% drop in Q1 earnings estimates during the last 60 days and a 4% drop in full-year FY27 earnings estimates.

Picture Supply: Zacks Funding Analysis

What traders might also need to remember is that whereas Houlihan inventory is buying and selling at an inexpensive 17X ahead earnings a number of, it is a sharp premium to its Zacks Monetary-Miscellaneous Providers Business common of 10X, with different noteworthy friends being American Categorical AXP), Coinbase COIN), and LendingClub LC).

Picture Supply: Zacks Funding Analysis

Backside Line

Houlihan Lokey stays a high-quality monetary funding financial institution with a powerful long-term monitor file, however the pattern of declining EPS revisions suggests short-term weak spot continues to be forward.

Till analysts see stabilization or a pickup in dealmaking or restructuring exercise, Houlihan’s inventory is more likely to stay underneath strain after falling practically 20% within the final six months.

Radical New Expertise May Hand Traders Enormous Features

Quantum Computing is the subsequent technological revolution, and it could possibly be much more superior than AI.

Whereas some believed the expertise was years away, it’s already current and shifting quick. Massive hyperscalers, corresponding to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Cook dinner reveals 7 fastidiously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s huge potential again in 2016. Now, he has keyed in on what could possibly be “the subsequent huge factor” in quantum computing supremacy. Right now, you’ve got a uncommon likelihood to place your portfolio on the forefront of this chance.

See Prime Quantum Shares Now >>

Houlihan Lokey, Inc. (HLI) : Free Inventory Evaluation Report

American Categorical Firm (AXP) : Free Inventory Evaluation Report

LendingClub Company (LC) : Free Inventory Evaluation Report

Coinbase World, Inc. (COIN) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.