Nvidia NVDA) as soon as once more reminded Wall Avenue why it stays the centerpiece of the substitute intelligence growth after delivering one other quarter of outcomes that crushed expectations yesterday night.

Nvidia’s Q1 outcomes highlighted simply how robust demand stays for its AI infrastructure merchandise because the chip big continues to profit from large spending by hyperscalers, cloud suppliers, and enterprises racing to construct out AI capabilities.

Posting surging income and earnings progress in Q1, Nvidia additionally strengthened confidence in its long-term trajectory by elevating its dividend and increasing shareholder returns by way of inventory buybacks.

For buyers trying to find a dominant progress inventory with bettering capital return insurance policies, Nvidia’s newest quarter made a compelling case.

AI Demand Continues to Gasoline Explosive Progress

Knowledge heart income remained the important thing progress engine, powered by demand for Nvidia’s GPUs and AI accelerators.Corporations creating massive language fashions (LLMs), generative AI purposes, and superior computing programs proceed to rely closely on Nvidia {hardware}.

This drove Q1 gross sales up 85% yr over yr to a document $81.61 billion, from $44.06 billion within the comparative quarter and impressively topping estimates of $78.39 billion by 3%. Knowledge Heart phase income surged 92% YoY with Nvidia CEO Jensen Huang calling the “buildout of AI factories the most important infrastructure enlargement in human historical past that’s accelerating at a unprecedented pace”.

Extra spectacular, Nvidia’s Q1 adjusted earnings of $1.87 per share surged greater than 140% from EPS of $0.77 a yr in the past and beat expectations of $1.70 by 10%.

Picture Supply: Zacks Funding Analysis

Moreover, administration issued robust ahead steerage, showcasing that AI demand stays sturdy regardless of considerations that spending may gradual after such a historic run.

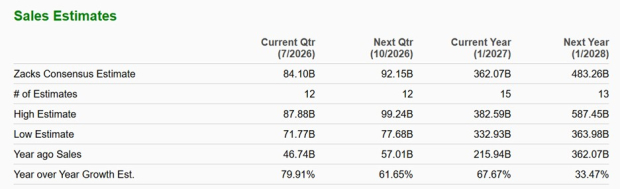

On this regard, Nvidia guided Q2 gross sales at roughly $91 billion plus or minus 2%, and properly above Wall Avenue’s consensus of $84.1 billion or practically 80% progress (Present Qtr beneath).

Nvidia additional famous that demand for its next-generation Blackwell programs stays exceptionally robust, indicating that AI infrastructure spending should be within the early innings slightly than nearing a peak.

Picture Supply: Zacks Funding Analysis

Nvidia’s Dividend Enhance Indicators Superior Confidence

One of many largest takeaways from Nvidia’s newest report was the corporate’s resolution to lift its quarterly dividend from $0.01 per share to $0.25 per share, representing an enormous 2,400% enhance.

Whereas Nvidia isn’t historically seen as a dividend inventory, the rise sends an necessary message to buyers: administration believes money flows have gotten more and more sturdy and sustainable.

Notably, Nvidia’s free money stream (FCF) surged 85% final quarter to $48.55 billion from $26.13 billion a yr earlier. In the meantime, the entire liquidity on Nvidia’s steadiness sheet spiked 50% YoY to greater than $80 billion when together with money & equivalents and marketable securities. These figures spotlight how aggressively Nvidia’s AI knowledge heart enterprise has been changing income progress into money era.

And for sure, corporations usually don’t increase dividends aggressively until management is assured about future profitability and steadiness sheet power. Nvidia’s skill to develop income at a unprecedented tempo whereas concurrently returning extra capital to shareholders demonstrates the immense monetary energy of its AI-driven enterprise mannequin.

The dividend enhance additionally broadens Nvidia’s attraction to a wider group of buyers. Progress-focused buyers are already drawn to the corporate’s AI management, however rising shareholder payouts might now entice long-term institutional and income-oriented buyers as properly.

Buybacks Add One other Tailwind

Nvidia additionally emphasised its dedication to shareholder returns by way of inventory repurchases, saying an extra $80 billion share repurchase authorization following its newest Q1 report.

The brand new authorization got here on high of roughly $38.5 billion remaining repurchases beneath the corporate’s earlier buyback program, bringing its whole licensed repurchases to roughly $118.5 billion.

Buyback applications might be particularly highly effective when executed by corporations producing monumental free money stream like Nvidia. Repurchasing shares reduces the entire share depend excellent, which may increase earnings per share over time and enhance possession stakes for current buyers.

For Nvidia, the buyback announcement reinforces a number of bullish factors:

- The corporate is producing substantial extra money.

- Administration believes the inventory nonetheless provides long-term worth.

- Nvidia can make investments closely in progress whereas additionally rewarding shareholders.

This is a crucial distinction as many high-growth know-how corporations prioritize enlargement on the expense of shareholder returns. Nevertheless, Nvidia is more and more displaying it could actually do each concurrently.

That mixture typically marks the transition from a fast-growing firm right into a mature know-how powerhouse.

Abstract & Conclusion

Nvidia’s stellar Q1 outcomes strengthened the corporate’s standing as probably the most highly effective progress tales out there at this time.

The tech chief is benefiting from extraordinary AI demand, increasing profitability, and massive free money stream era. Extra importantly for buyers, Nvidia is now pairing that progress with stronger shareholder return initiatives by way of dividend will increase and inventory buybacks.

That mixture makes Nvidia look more and more engaging not simply as an AI progress inventory, but additionally as a long-term compounder able to rewarding shareholders in a number of methods. In the meanwhile, Nvidia inventory at the moment sports activities a Zacks Rank #2 (Purchase) based mostly on a development of favorable EPS revisions that appears prone to proceed.

Zacks’ Analysis Chief Names “Inventory Most Prone to Double”

Our workforce of consultants has simply launched the 5 shares with the best likelihood of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This high decide is a little-known satellite-based communications agency. House is projected to develop into a trillion greenback trade, and this firm’s buyer base is rising quick. Analysts have forecasted a significant income breakout in 2025. After all, all our elite picks aren’t winners however this one may far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our Prime Inventory And 4 Runners Up

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.

2026-05-21")